Homepage | About us |

Advertise | Partners |

Contacts | Contacts |

Русский Русский

|

|

|

|

Latest News

Recent Comments

|

Lack of legislation hinders Islamic finance march in Russia08.06.2010Moscow: There is no doubt of the potential for Islamic finance in Russia and the CIS countries, but the major stumbling block is the absence of enabling legislation and a regulatory framework to facilitate Islamic financial products such as Murabaha, Ijara and sukuk.

Mushtak

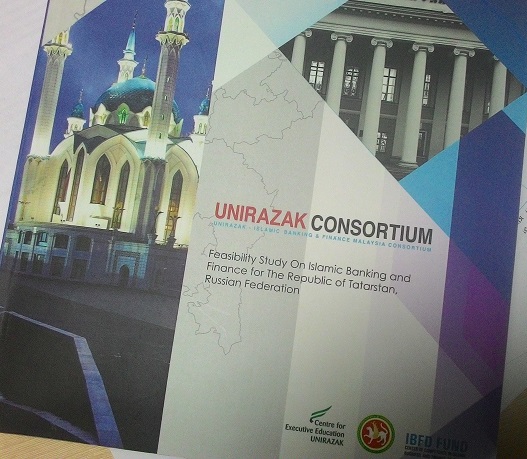

Parker Moscow: There is no doubt of the potential for Islamic finance in Russia and the CIS countries, but the major stumbling block is the absence of enabling legislation and a regulatory framework to facilitate Islamic financial products such as Murabaha, Ijara and sukuk While the Central Bank of Russia largely remains disinterested in taking the initiative in facilitating Islamic finance in the country, behind the scenes there are some encouraging developments which could speed up the introduction of Shariah-compliant products there. Given the federal system in Russia, there are ways of bypassing the Central Bank of Russia’s inertia. For instance, the government of the Russian autonomous republic of Tatarstan, which is Muslim dominated, has got presidential blessing to open up to the sector. In fact, the Islamic Development Bank recently confirmed a $1 million equity stake in the Islamic Investment Company of Tatarstan (IICT), a joint venture established with two government entities. IICT will effectively be overseen by the Islamic Corporation for the Development of the Private Sector (ICD), a member of the IDB Group, and according to Khaled Al-Aboodi, CEO of ICD, IICT will identify projects and transactions for which the ICD will try to find investors from its member countries. These would be targeted toward small-and-medium-term enterprises (SMEs). In fact, Tatarstan is hosting a major Islamic finance investment symposium in Kazan in two weeks time. Other Muslim Republics in Russia such as Dagestan, Chechnya, Ingushetya and others could equally follow the same route, subject to instilling greater awareness and market education regarding Islamic finance. Another potentially important development is the establishing of a task force on alternative (Islamic) financial institutions and products by the influential Association of Regional Banks of Russia. "Our mandate is to come up with a draft legal and regulatory framework for alternative Islamic financial institutions and products which we could then present to the various political and financial powers that be for further consideration and recommendations. We have approached three of the big four advisory firms to help in this respect and we will choose which route to go once we have their initial input. This process could take the next few weeks, I believe,” explained Alexei G. Kovalenko, head of the task force. Kovalenko, a former banker and insurance executive, has some experience in Islamic finance, having established the first Takaful company in New Zealand a few years ago. Major Russian banks such as VTB (Vneshtorgbank) and Gazprombank also confirm that they are working on Islamic financial products albeit originated outside Russia. Stanislav Yankovets, managing director, strategic development , Middle East and North Africa, confirmed to Arab News that VTB Capital, a wholly-owned subsidiary of VTB, has resumed work on issuing a sukuk through its Dubai entity VTB Capital Dubai. "We were working on a possible sukuk issuance in 2008, but then the financial crisis happen and everything was put on hold. But now we have resumed work on the possible issuance of a sukuk. We have signed an agreement with Kuwait Finance House, which will help seed the issuance and help with the distribution,” explained Yankovets. Similarly, Gazprombank, according to Michel Cordahi, head of Capital Markets, is similarly looking at structuring Islamic capital market products and raising funds through a sukuk issuance through its Lebanese subsidiary Gazprombank Invest (MENA) SAL. At the same time Azerbaijan’s largest bank, the International Bank of Azerbaijan (IBA), stressed Azer Safarov, adviser to the chairman of the board of IBA, is in the process of setting up an Islamic Banking Window and plans to offer Islamic financial products especially Murabaha trade finance and Ijara leasing and consumer finance through its Moscow branches to customers in Russia and the region. Indeed, the IAB is also a major driver behind the establishment of the Islamic Banking and Finance Council (IBFC) of the CIS, the first regional professional body to serve the sector. Safarov, confirmed to Arab News that the articles of formation of IBFC was submitted a few days ago to the Russian Ministry of Commerce for registration and approval, a process which normally takes a few weeks. Further evidence of greater interaction of Russian entities with overseas counterparts is the two memoranda of understanding (MoUs) signed in Moscow during the Forum by Al-Shams Capital, an asset management company authorized by the Securities Commission of Russia but which operates exclusively under Shariah investment principles. The first MoU was signed with Theissen Law and Lux Global Trust Services — both from Luxembourg- whereby the three parties would cooperate toward the establishment of a CIS incubator private equity fund which would be domiciled in Luxembourg and which would primarily be aimed at investing in SME halal-related business activities including medium-sized financial institutions (Islamic banks, leasing companies, Takaful companies), companies involved in halal food production and distribution etc. The agreement was signed by Adalet Djabiev, CEO of Al-Shams Capital, and Marc Theissen, senior partner, Theissen Law in the presence of Gaston Stronck, the ambassador from Luxembourg in Russia. The second MoU was with Oasis Holdings (PTY) Ltd. of South Africa, whereby the two parties agree to work toward forging a strategic alliance in identifying potential business opportunities and providing Islamic asset management services in Russia and the CIS countries, and toward potentially establishing a private equity fund management service with Al-Shams Capital. Adalet Djabiev signed on behalf of Al-Shams and Nazeem Ebrahim, vice chairman of Oasis signed on behalf of the South African Group, which has a stable of 63 Islamic funds, the third largest universe of Shariah-compliant funds in the world after Malaysia’s 155 and Saudi Arabia’s 141. The general consensus was that the potential for Islamic finance is huge in Russia and the CIS countries but the lack of enabling legislation and the regulatory framework to facilitate such products would hamper its rapid introduction in the Russian market. In the aftermath of the financial crisis, emerging countries such as Russia are looking toward alternatives to market capitalism, and Islamic finance with its emphasis on financing the real economy as opposed to speculative activities such as derivatives ought to be well-placed. Sergey Pakhomov, chairman of the State Debt Committee of the City Government of Moscow, stressed that the City raises in excess of $5 billion of financing from the international markets. More recently, the City Government has explored the issuance of sukuk as part of its source of funding diversification strategy. While the interest in issuing the sukuk is there, the current Russian legal structure is simply not in place to facilitate such an issuance. For instance, Russia has no trust or SPV laws, let alone tax neutrality measures in place. He was also concerned by the implications and fallout of the AAOIFI statement on sukuk , but is confident that Islamic capital markets products has huge potential in Moscow, Russia and the CIS region. Murabaha is a contract for purchase and resale, when a bank purchases the goods for the customer and resells them on a deferred basis, adding an agreed profit margin. Ijara is a form of a lease contract, when the finance provider buys the property at a fixed price then leases it to the customer, in return for rental payments over a fixed period. Sukuk are certificates of equal value, Sharia compliant bonds. The sukuk holders are entitled a profit generated by the underlying assets as well as to proceeds of the realization of the assets ArabNews

Latest News |

Editor's Column Analytics

News in RSS format |

| © IBFD Fund, 2009-2026. Developed by Linova-MEDIA. Хостинг от uCoz. Design by WebRT |